“Most of our assumptions have outlived their uselessness.”

― Marshall McLuhan

“Assumptions are dangerous things to make, and like all dangerous things to make ― bombs, for instance, or strawberry shortcake ― if you make even the tiniest mistake you can find yourself in terrible trouble. Making assumptions simply means believing things are a certain way with little or no evidence that shows you are correct, and you can see at once how this can lead to terrible trouble. For instance, one morning you might wake up and make the assumption that your bed was in the same place that it always was, even though you would have no real evidence that this was so. But when you got out of your bed, you might discover that it had floated out to sea, and now you would be in terrible trouble all because of the incorrect assumption that you'd made. You can see that it is better not to make too many assumptions, particularly in the morning.”

― Lemony Snicket, The Austere Academy

In a blogpost which is titled ZimAsset: The Things That Haven't Been Said and The Numbers You've Never Seen, I discussed the insurmountable hurdles that the architects of ZimAsset would need to overcome, including:

- Idiosyncratic Factors and Political Realities.

- Funding Constraints and Realities of the Global Economy.

- Debt Sustainability Issues.

Evidently, the hurdle that lies outside the sphere of influence of the architects of ZimAsset is Funding Constraints and Realities of the Global Economy.

As I alluded to in the blogpost which is titled ZimAsset: The Things That Haven't Been Said and The Numbers You've Never Seen, the key constituent of this particular hurdle is China's demand for commodities.

Stated otherwise; any adverse change in China's demand for commodities would, in essence, be a headwind that would have a negative bearing on the implementation of ZimAsset. Illustration 1, below, depicts this, and another, headwind:

|

| Illustration 1 (click on illustration to zoom in) |

- Lie outside the sphere of influence of the Zimbabwean government.

- Would have a negative bearing on the implementation of ZimAsset.

To expound on the headwinds in Illustration 1:

- The Global Commodities Supercycle: Over the last twenty years, the upsurge in global commodity prices was largely driven by China's demand for commodities (particularly energy commodities and base metals). This demand was, in turn, spurred by China's growth model which was driven by: 1) Exports of manufactured goods, and, 2) Fixed capital investments. In a blogpost which is titled China's Edifice Complex: Shadow Banking, Debt Bubbles and Mining Opportunities in Africa, I discussed how this growth model had run out of steam. Further, in a subsequent blogpost which is titled ZimAsset: The Things That Haven't Been Said and The Numbers You've Never Seen, I discussed how China's policymakers intended to supplant the fixed-investment-and-export-led growth model with a more sustainable domestic-consumer-spending-led growth model. Furthermore, in the latter post, I also discussed how this change in China growth model would: 1) Cut China's demand for commodities, which would; 2) Ignite a secular decline in global commodities prices, and; 3) Adversely affect the natural resource-centered aspects of ZimAsset. At the just-ended 2014 Milken Institute Global Conference, Dr. Nouriel Roubini (also known by the following moniker: "Dr. Doom") stated, and I quote: "The reality is that while they [Chinese policymakers] do realize that their growth model is unsustainable and uncoordinated as they say; fixed investment is 50% of GDP; savings more than 15% of GDP and consumption only 35% of GDP. The re-balancing from one to the other, in my view, is going to occur much more slowly than is desired and optimum. Because of two reasons. One: is that the interest groups that are in favor of the old growth model are very powerful; state-owned enterprises, provincial governments, their SPVs [Special Purpose Vehicles], the PLA [People's Liberation Army] and the state sector. While those who are going to be benefiting from a growth rate that is consumption-oriented and labor intensive ― workers and households ― are politically not strong because it [China] is not a democracy. Secondly, when I was, in November, in China, on delegation, I met both the President, Xi, and the Prime Minister, Li, and both of them said; 'It's a utmost [sic] our goal to have 7.5% growth during this decade. Because we have an objective to double GDP by the end of the decade'. It's a political objective. But if you are really serious about the re-balancing and stopping this build-up of credit; every time growth slows down towards 7%, in the last five years, they have gone into a panic and done another round of credit-fueled fixed investment. That means: more bad assets ― in the banks and the shadow banks; more NPLs [Non-Performing Loans]; more bad investment ― in real estate in infrastructure, in industrial capacity ― which is already excessive; and more debts that, both in the private and public sector are excessive. The leverage ratio right now in China 240% [of GDP] and rising, between private and public [sector] debt (sic). That eventually is going to lead to a hard landing. To me, a hard landing is not 3% or 4% growth. But I think that by next year [2015] growth is going to be 6%, and the next year [2016] it's going to be lower than 6%. That is not hard landing, and that is not the consensus soft landing". Succinctly put: Dr. Nouriel Roubini states that; owing to vested interests, the anticipated reorientation of China's growth model may not occur in the near-term. Therefore, this implies that in the near-term China's pace of fixed capital investment will remain unchanged. Further, this also implies that her export-led growth model would only be disturbed by lack of global demand. Otherwise stated; in the near-term, commodity prices may not dip because of falling Chinese demnd. However, in the medium-to-long term, the change in China's growth model poses the greatest downside risk to global commodity prices. Thus, it is reasonable to assert that the Global Commodities Supercycle headwind remains a threat to the architects of ZimAsset in the medium to longer term. This is depicted by the weaker headwind labelled 1 in Illustration 1.

- Extraterrestrial Sources of Platinum Group Metals and Energy Minerals: This factor is depicted by the stronger, larger and more proximate headwind which is labelled 2 in Illustration 1. And, it will be discussed in the forthcoming sections of this post:

***

One of the highlights of the just-ended 2014 Milken Institute Global Conference was a panel discussion which was christened Why Tomorrow Won’t Look Like Today: Things that Will Blow Your Mind. The panelists included:

- Eric Anderson the Co-Founder and Co-Chairman of Planetary Resources.

- Eric David the Co-Founder and Chief Strategy Officer of Organovo.

- John Kelly III the Senior Vice President and Director of IBM Research.

In this post, I'll focus on the presentation that was made by Eric Anderson of Planetary Resources:

In November of 2010, Planetary Resources was established by Peter Diamandis (of the X-Prize fame), Erick Anderson and Chris Lewicki.

Currently, the organization has a team of forty PhD-level engineers. Noteworthily, some of the members of Planetary Resources's team were constituents of the Nasa Jet Propulsion Lab (JPL) unit that landed a probe on Mars.

Curiously, the company has a bland mission: to "expand the Earth's natural resource base". Interestingly enough, this mission masks the complexity of the vector that the company will take to this envisaged end-state: extracting mineral resources from extraterrestrial bodies, like asteroids.

Illustration 2, below, is a picture of an asteroid:

|

| Illustration 2 (click on illustration to zoom in) Adapted From: Crystalinks, 2014 |

Essentially, asteroids are remnants of the early solar system. They are chemically equivalent to the material that lies at the planetary core of Earth.

Generally, asteroids are located in a heavenly zone that lies between Mars and Jupiter. As Illustration 3, below, shows, this region is known as the Asteroid Belt:

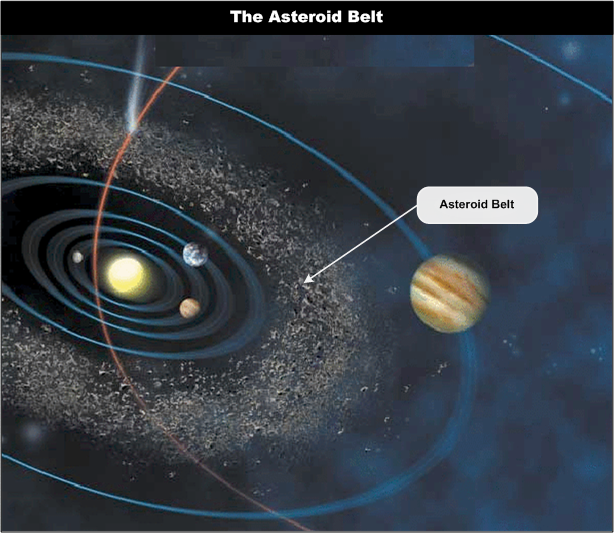

|

| Illustration 3 (click on illustration to zoom in) Adapted From: World Mysteries, 2014 |

In the Asteroid Belt, there are between 60 and 100 million asteroids. Intriguingly, the aggregate mass of these asteroids is equivalent to, at least, the mass of an Earth-sized planet. As it currently stands, we've only discovered 1% of the asteroids in the Asteroid Belt.

Generally, there are over 10,758 asteroids that equidistant to Earth as the Moon. By and large, some of these asteroids travel in similar orbits as Earth. Tellingly, these asteroids are known, in astronomical parlance, as near-Earth asteroids. [1]

It is the mineral wealth that is contained in these proximate asteroids that Planetary Resources seeks to tap. Naturally, this begs the question: How much mineral wealth is in one asteroid? Generally:

- An asteroid contains Platinum Group Metals. These minerals can be found at concentrations that average 10,000 times the concentrations of the richest platinum mines on Earth. To put this into context;

- An asteroid with a volume of approximately 2,500 cubic meters would have approximately USD600 billion-worth of Platinum Group Metals (valued at current prices). This suggests that the average near-Earth asteroid has about USD240 million-worth of Platinum Group Metals per cubic meter.

- The Platinum Group Metals that are found on asteroids are twenty-five times the density of water.

- The non-Platinum-Group-Metal constituents of asteroids, i.e. the volatile materials on asteroids, are one of the most energy efficient materials known to mankind (when you break them down into hydrogen and oxygen). According to some estimates, asteroids may have up to USD50 million of rocket fuel per tonne.

Succinctly put; asteroids are replete with metals and energy materials.

***

Heretofore, the mineral wealth of asteroids was inaccessible because of expense:

Interestingly, the key innovation that Planetary Resources brings to bear is cost; the company is implementing a cost leadership strategy. More precisely put; Planetary Resources has brought down cost of sending a (small) droid into deep space from USD250 million to USD2 million. By and large, the components that Planetary Resources uses are one hundredth the cost of the components that were used by other space missions.

Hence, it is reasonable for one to conclude that Planetary Resources's cost disruptions have: 1) Opened-up a new frontier of resources, and; 2) Enabled humanity to become a space-ferrying species.

Naturally, this begs the question of when Planetary Resources will start having a disruptive impact on the extraction of Platinum Groups Metals. The timeline in Illustration 4 has the answer:

|

| Illustration 4 (click on illustration to zoom in) Adapted From: Anderson, 2014 |

As Illustration 4 shows, Planetary Resources will start to have a disruptive impact on the Platinum Metal Group industry between 2016 and 2017; i.e. two to three years from now.

To provide an illustrative example of the possible scale of the disruption: During the 18th century aluminium was the most expensive metal.

Why? Because;

- Aluminium is extremely rare in its purest form.

- The contemporaries did not have the technology to separate aluminium from its ore, bauxite.

In fact, in the 18th century, aluminium was so rare (and valuable) that important visiting dignitaries to the court of the French King would be served on a table with fine aluminium cutlery; while the nobles were served on a table with golden cutlery.

As recently as 1890, aluminium was priced at $33 per kilogram (which translates to a price of $888.51 per kg in 2014 dollars). After the Pittsburgh Reduction Company started commercial production of aluminium, using the Hall-Heroult process, the price of aluminium plummeted to $1 per kilogram (which translates to a price of around $26.92 per kg 2014 dollars).

I firmly believe that Planetary Resources will have a disruptive impact (of a similar order of magnitude) to the Platinum Metals Group industry.

For Zimbabwe, this implies:

- That its untapped Platinum Group Metal wealth would become worth less (not worthless);

- The communities that entered into the "vendor-financed" empowerment deal with Zimplats will never realize the benefits of owning a stake in the company.

Clearly, the architects of ZimAsset made the mistake of assuming that tomorrow will look like yesterday and today. Evidently, they did not factor in the impact of industries of the future like; Energy Technology (Shale Gas), Biotechnology (Stemcell Therapy), IT (Bigdata and Autonomous Robotics), New Manufacturing Technology (Nanotech) and Defense Techonologies (Drones).

The mistake that they made may prove to be costly.

[1] For more information on asteroids visit this Planetary Resources blogpost.

[1] For more information on asteroids visit this Planetary Resources blogpost.