Direct frontier markets investment is associated with a host of risks, of which expropriation is the most prominent. [4]

In this post, I will outline an approach that could be used to estimate expropriation risk. Further, I will also discuss the dynamics of expropriation using: the J-Curve; a conceptual tool that was developed by Ian Bremmer, and; the assertions that I drew from Bruce Bueno De Mesquita and Alastair Smith's text entitled "The Dictator's Handbook".

***

The questions that would be used to shape this blog post can be abbreviated as follows:

- When does expropriation occur?

- What are the drivers of expropriation?

When does expropriation occur?

The following quote, from David Landes's text entitled "The Wealth and Poverty of Nations", has got clues on the political conditions that amplify the risk of expropriation:

"In despotisms, it is dangerous to be rich without power. It arouses cupidity

and invites seizure."

- David Landes (The Wealth and Poverty of Nations)

From the assertion that was made by David Landes, one can infer that the risk of expropriation increases in conditions of despotism, i.e. where political power is repressive and concentrated. The concentration of political power in a society can be estimated by employing the following "selectorate index": The number of people who are eligible to vote under the laws of a nation divided by The number of people who would be eligible to vote if the nation adopted international standards of democracy and universal suffrage. [1]

Hence, the abovementioned inference and supposition can be used to plot the following graph:

|

| Illustration 1: Click on illustration to zoom in |

In Illustration 1, the movements upwards and to the left, depicted by red arrows, indicate an increase in expropriation risk. The greatest increase in the general expropriation risk is depicted by the movement from Quadrant 2 to Quadrant 1. The move from Quadrant 3 to Quadrant 1 indicates an increase in the probability of a mass revolt and an increase in the expropriation risk of politically well-connected entities. And, the movement from Quadrant 4 to Quadrant 3 represents a moderate increase in the short term risk of expropriation; however,the move is usually ensued by the movement from Quadrant 3 to Quadrant 1 - so it represents a high increase in the risk of expropriation within a 3 to 5 year period. [8]

The conceptual framework in Illustration 1 can be supplemented by the adaption of Ian Bremmer's J-Curve in Illustration 2:

|

| Illustration 2: Click on illustration to zoom in |

I'll start by explaining the general concept of the J-Curve, by using an excerpt from "The J-Curve" book press release: "If you take a cross section of nations and measure

each one’s stability in relation to its political and economic openness to the

outside world, and then plot the resulting data points on a graph, the result

is a curve shaped like a J. Nations to the left of the dip in the J are less

open; nations to the right are more open. Nations higher on the graph are more

stable; those that are lower are less stable. Movement from left to right along

the J curve demonstrates that a country that is stable because it is closed

must go through a period of instability as it opens to the outside world."

To give the conceptual framework in Illustration 2 practical utility, the following proxies can be employed:

- Percentage Change in Exports for Openness.

- Percentage Reduction in Incidents of Social Unrest for Stability.

- Expropriations occur when a country is starting to become more open: When a country is starting to become more open stability falls, as it moves up the J-Curve. In Illustration 2, this is illustrated by the move towards point a from the left hand side of the J-Curve. Usually, when this shift occurs, the entities that were closely associated with a deposed autocratic regime stand the risk of expropriation.

- Expropriations occur when a country is increasingly becoming more closed: When a country is becoming more closed, stability falls as it moves down the J-Curve. In illustration 2, this is illustrated by the move towards point a from the right hand side of the J-Curve. Usually, when this happens, the following entities face the risk of expropriation: Foreign entities, Entities that were closely associated with a deposed political faction/party and Entities from sectors of the economy that are of the most importance and generate the most revenue (in forex terms).

What are the drivers of expropriation?

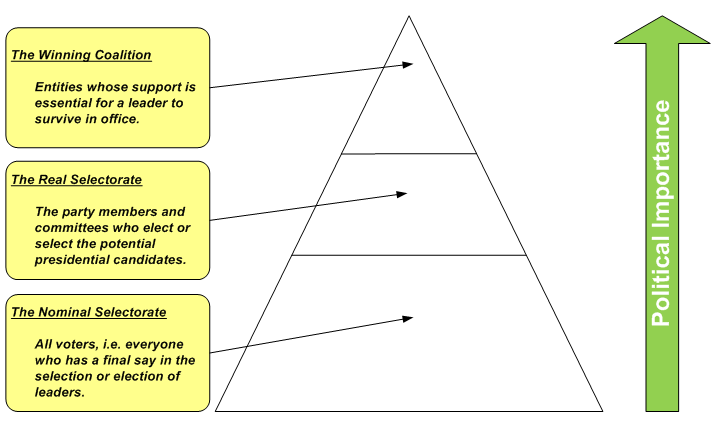

In their text entitled "The Dictator's Hand Book", Bruce Bueno De Mesquita and Alastair Smith state that there are generally three constituencies of political importance in a society [2]: The Nominal Selectorate, The Real Selectorate and The Winning Coalition. Illustration 3 below describes the constituencies, and, it positions them in terms of their political importance to an incumbent political leader:

|

| Illustration 3: Click on illustration to zoom in |

According to De Mesquita and Alastair, an incumbent politician's chief concern is to stay in power. To stay in power, a politician requires the support of The Real Selectorate and a subset of The Real Selectorate that they term The Winning Coalition (see Illustration 3). This support is, according to the authors, essentially "bought with money".

Therefore, it is reasonable to assert that the risk of expropriation of an entity increases when:

- The support base of an incumbent is dwindling: When this happens, the price of the support of The Real Selectorate increases, i.e. it would take more money to get them to rally behind an incumbent. If additional funds can only be accessed with more effort than the effort that is required to expropriate assets, the incumbent will do the logical thing: expropriate assets.

- When The Real Selectorate grows: When this occurs, more money is needed to buy the support of an increased number of key people. Again, if additional funds can only be accessed with more effort than the effort that is required to expropriate assets, the incumbent will do the logical thing: expropriate assets.

- When a country is undergoing financial hardship: Traditional sources of funds dry-up and new sources of funds need to be secured to buy the continued support of The Winning Coalition. The said "new sources of funding" may be the expropriated assets that are owned by "dispensable entities".

- When political rivals can make better offers to The Real Selectorate: An incumbent would be forced to make a higher bid. And, this naturally requires more money. Again, if additional funds can only be accessed with more effort than the effort that is required to expropriate assets, the incumbent will do the logical thing: expropriate assets.

- The entity is a marginal member of The Real Selectorate: According to De Mesquita and Smith, incumbents prefer a Winning Coalition that is as small as possible. They periodically cull-out members of The Winning Coalition who: 1) Have the power to depose them; 2) Have got questionable loyalties; 3) Have got great abilities and ambitions, and; 4) Are dispensable. [5].

Dokolo - wealthy beyond the dreams of avarice

In the late 1960s, there lived, in Zaire (now called the DRC) a man called Augustin Dokolo Sanu. He was wealthy beyond the dreams of avarice and he had interests in Banking (The Bank of Kinshasa), Agriculture, Food Processing, Car Dealing, Mining, Transport, Printing, Insurance Brokerage, Customs Clearance, Real Estate and Trading.

By all accounts, Dokolo's empire aroused both admiration and envy. Just about every prominent member of the Zairean society wanted to be associated with him. Between the 1960s and the 1980s, Dokolo was offered numerous public sector positions. Being the time pressed man he was, he always declined by saying that he didn't have enough time to focus on anything that was not related to his business interests.

Dokolo's wealth largely depended on a strong copper price. And, when the demand for copper started to soften, most of his bank's debtors, copper miners, found it difficult to service their debt. Owing to this, support from the central bank was needed to enable The Bank of Kinshasa to fulfil its commitments to foreign creditors.

Around 1985, The Bank of Kinshasa (BK), was charged onerous "new" interest rates for borrowing from the Zairean central bank. These interest charges (including the principal) amounted to 97% of Dokolo's "revised" networth (i.e. According to the valuations of the Zairean central bank; which accused him of using his real estate company to inflate the valuations of his assets [7]). Unbeknownst to Dokolo, these new interest rate charges and revised valuations were to mark an inflection point in the trajectory of the Dokolo empire.

As fate would have it, Dokolo didn't have enough liquid assets to cover the predatory interest charges. Naturally, this put depositors' funds at risk. Thus, he was forced to surrender the majority of his personal fortune as surety and his bank went into "indefinite" administration; i.e. he never got his bank back and he never got back the assets that were surrendered as surety [6]. The long and short of it is: his assets were nationalized by the government of Mobutu Sese Seko.

Mobutu is the man who once said something that lends credence to the assertion that was made by De Mesquita and Smith (i.e. the assertion that political leaders buy the support of key constituencies with money), and I quote:

I think the quotation has got clues on what Dokolo's expropriated wealth was used for...

"What is important here is cash. [A] leader needs money, gold and diamonds to run his hundred castles, feed his thousand women, buy cars for the millions of boot-lickers under his heels, reinforce the loyal military forces and still have enough change left to deposit into his numbered Swiss accounts."

***

[1] It is important to point out that this formula is a crude method of estimating the concentration of power in a society and it was merely used for illustrative purposes.

[2] Bruce Bueno De Mesquita is an academic and a consultant with the C.I.A. He developed a computerized system that is underpinned by Game Theory and Graph Theory; the system can predict future events that involve complex negotiations between numerous entities. And, according to the C.I.A, the system has got a 90% accuracy rate when it comes to predicting events that occur on the global geopolitical landscape. Because of this, people call Bruce a modern Nostradamus.

[3] The authors' assertions are underpinned by rigorous quantitative and qualitative analyses, and, they are backed up by empirical evidence from across the globe. Please read the book, in its entirety, before you dismiss these assertions.

[4] According to Investopedia, expropriation is "the act of taking of privately owned property by a government to be used for the benefit of the public".

[5] The first step is usually an arrest or legal proceedings. The second step in culling-out the named entities is usually financial dismemberment via expropriation.

[6] Dokolo never recovered from the expropriation of his assets; he spent the remainder of his life in mourning.

[7] It is almost impossible to verify whether this charge had any substence.

[8] These are generalizations. Contextual information is needed to interpret the true implications of these shifts.