"When it comes to the future, the only thing one can be sure of is that common sense will be wrong."

― George Friedman (The Next 100 Years)

"To him or her who looks upon the world rationally, the world in turn presents a rational aspect. The relation is mutual."

— George W. F. Hegel

"The twenty-first century will be like all other centuries. There will be wars, there will be poverty, there will be triumphs and defeats. There will be tragedy and good luck. People will go to work, make money, have children, fall in love, and come to hate. That is the one thing that is not cyclical. It is the permanent human condition."

― George Friedman (The Next 100 Years)

Over the last week, I was prompted, by the currently-unfolding Russia-Turkey spectacle, to re-read one of my favorite texts of all time which is titled The Next 100 Years: A Forecast For the 21st Century. The text was authored by Dr. George Friedman ― the founder of the Geopolitical Intelligence firm, Stratfor ― in 2009.

In the text, Dr. Friedman made prescient predictions of the following events:

- Russia's Westward Territorial Expansion: He predicted the Russian annexation of Crimea and Russia's invasion ― via the stimulation of ethnic Russian Ukrainian separatists ― of Eastern Ukraine. [1]

- China's Economic Slowdown: He also accurately predicted the slowdown of the Chinese economy, and, he foresaw the advent of a financially-debilitating non-performing loan cycle. The non-performing loan cycle is presently rearing its hideous head, and, it is set to reach a crescendo between 2017 and 2020. [2]

- Russia-Turkey Antagonisms: Dr. Friedman predicted the currently-unfolding confrontation between Russia and Turkey. [3]

When I read each prediction anew, I was haunted by the following thought: 'Does this prediction foreshadow doom and gloom for Africa, or, does it portend an era of stability and plenitude?'. In this blog-post, I will share the results of the thought exercise which was prompted by this question.

I will start by discussing the building blocks of my thought exercise. They include:

- Basic Element 1 which is a discussion of how the world (and Africa) really works.

- Basic Element 2 which is a discussion of the most basic growth paths for African economies to follow.

This discussion will pave way for a thematic exploration of the major first-order and second-order events that I foresee transpiring in Africa. The themes that will be used to structure this part of the blog post include:

- The Water Scarcity Problem.

- The Ever-Present Pandemic Risk.

- The Technological Dystopian Scenario.

- The 1980s Redux: The Balance of Payments Blip.

- The Demographic Conflagration.

- The Great Transition of China and its Shock Waves.

- The Aftermath of the Second Cold War.

The goals that underpin the authorship of this blog post are best explained by quoting the words of Dr. George Friedman: "I am simply trying to transmit a sense of the future. I will, of course, get many details wrong. But the goal is to identify the major tendencies — geopolitical, technological, demographic, cultural, military — in their broadest sense, and to define the major events that might take place."

***

...Basic Element 1: How The World (and Africa) Really Works

"Ever since the Civil War, the United States has been on an extraordinary economic surge. It has turned from a marginal developing nation into an economy bigger than the next four countries combined. Militarily, it has gone from being an insignificant force to dominating the globe. Politically, the United States touches virtually everything, sometimes intentionally and sometimes simply because of its presence... The argument I’m making is that the world does, in fact, pivot around the United States."

― George Friedman (The Next 100 Years)

"The American empire comprises 17 percent of the world’s population but controls about 70 percent of the gross world product. Because nearly all of the developed countries are included, the network’s share of science, technology, and corporate resources is closer to 90 percent of the world’s total.”

― William E. Odom and Robert Dujarric (America’s Inadvertent Empire)

In Martin Meredith's 5,000-year history of the African continent, the following themes are evident [5]:

- Soft and Hard Commodities: Throughout the sweep of African history, the basis of the continent's relationship with the rest of the world has been commodities; gold, ivory, rubber, commoditized labor (slaves), wheat, base metals, energy commodities and other soft and hard commodities. This assertion simply implies that: 1) All relations, past and present, between Africans and external parties are buttressed by external parties' need for African commodities, and; 2) Commodity markets are the channel through which world events and trends are transmitted to Africa.

- Tribal Loyalties: Ethnic loyalties and filial piety transcend loyalties to state, global ethical standards and conventional notions of human rights. Most of the conflicts that occurred in Africa were the logical extreme of fidelity to ethnicity; they were dystopian expressions of impulses of kinship. [6]

- Geographical Constraints: The developmental constraints that geography has placed upon the African continent can be summed as follows: 1) Uneven rainfall patterns that hinder the effective development of agriculture; 2) A tropical environment which is conducive to the spread of pestilence and vermin; 3) Fragile clayey soils that degrade with great ease and rapidity, and; 4) Scorching heat. Where technology has been adopted quickly and developed, these constraints have been reasonably tamed and economic development is occurring at an encouraging pace. Conversely, where technology has been sluggishly adopted and developed, these constraints continue to torment the populace with morbidity, squalor and food insecurity. Key to the adoption of appropriate technologies that were developed elsewhere is the accessibility of a polity's home terrain ― a gift of geography ― and an open culture [7] [19].

- External Agency: The interests and actions of 'external parties' are a pivotal determinant of the development trajectory of Sub-Saharan Africa. They trump the interests and actions of 'internal parties'.

To expound on External Agency; The force that currently shapes the economic trajectory of African economies is the United States' Credit Cycle and the United States' appetite for imported goods and services. [26]

Illustration 1 ― below ― shows the trajectory that was followed by the World's GDP Growth Rate and the growth rate of U.S. Credit Market Instruments issued between 1960 and 2014:

|

| Illustration 1 (click on illustration to zoom in) Adapted From: Duncan, 2012; World Bank, 2015A, and; St Louis Fed, 2015 |

As Illustration 1 ― above ― shows, the curve of the World's GDP Growth Rate is almost identical to the curve of the US's Credit Market Instruments' Growth Rate; in fact, they appear to move in tandem.

From Illustration 1, it is clear that the behavior of the US Credit Markets Instruments' Growth Rate curve can be used to establish future zigs and zags in the World's GDP Growth Rate. Succinctly put; the credit creation process in the United States drives the World's GDP Growth Rate [8]. This naturally begs the question of how. Illustration 2 ― below ― provides the answer:

|

| Illustration 2 (click on illustration to zoom in) Adapted From: Duncan, 2012; World Bank 2015A, and; World Bank 2015B |

As Illustration 2 ― above ― shows, the US's Current Account Balance has an inverse relationship to the World's GDP Growth Rate. Otherwise put; the world economy grows when: 1) the US uses the proceeds of its credit creation process to run trade deficits (i.e. uses debt to import more goods than it exports), and; 2) when it makes transfers of funds abroad (e.g. fungible aid). The converse is also true.

Illustration 3 ― below ― presents the chain of causation that links some of the elements that were presented in Illustrations 1 and 2:

|

| Illustration 3 (click on illustration to zoom in) Adapted From: Duncan, 2012, and; Stacey et al., 2000 |

Illustration 3 ― above ― shows how the world's debt-based monetary system works; it all begins with US credit creation and imports. African countries have grown by either or both of the following vectors:

- Direct Exports to the U.S.: Exporting commodities and goods directly to the United States. This growth strategy requires a direct bilateral relationship with the U.S. For this relationship to have longevity and yield tangible results, African governments would have to show consistent progress towards democratization, upholding conventional norms of human rights and the adoption of the Washington Consensus.

- Supply Chain Linkages: Exporting primary and intermediate goods to countries, like China, that beneficiate them and export the finished goods to the U.S. This has been the most popular avenue of growth for the bulk of African governments as it insulates them from US / Western 'interference in their internal affairs' [9]. Most of the Africa Rising story can be traced to growth which was triggered by windfalls that stem from commodity exports to China.

...Basic Element 2: The Basics of Economic Growth in Africa

There are four obvious strategies that can be employed to bolster a nation's economic growth. They are depicted in Illustration 4 below:

|

| Illustration 4 (click on illustration to zoom in) Adapted From: Krugman, 1994 |

- Stage 1 - High School Education: This growth strategy is best-suited to economies that are emerging from a protracted military conflict, like the DRC. Equipping people with basic numeracy and literacy skills allows them to become more productive. With basic literacy skills: 1) Subsistence farmers are able to follow written instructions on pesticide containers which, consequently, enhances crop yields and food security; 2) Couples are able to effectively use, without family planning nurses, family planning methods which, consequently, allows them to have smaller manageable families and spend more limited resources per child; 3) Petty superstitions are eradicated and people are more amenable to using healthcare facilities which, consequently, eradicates morbidity; etc. Evidently, equipping people with basic literacy and numeracy skills bolsters economic growth and unleashes a tidal wave of second and third-order socio-economic benefits.

- Stage 2 - Rural-to-Urban Migration: In theory, rural-to-urban migration should move a nation's populace from low-productivity agricultural occupations to high-productivity industrial and service sector occupations. This should directly bolster economic growth. Further, rural-to-urban migration should alleviate land-pressure in rural areas and allow for rural micro plots to be consolidated into more productive large-scale lots. This should, in turn, enhance food security and bolster economic growth. In reality, African countries have failed to create viable urban industrial sectors. Further, China has become the factory of the world; it has out-competed the most notable remnants of Africa's industrialization experiments of the post-independence era. Thus, African rural-to-urban migrants are increasingly being met with few viable urban employment alternatives.

- Stage 3 - Fixed Capital Investments [25]: The goal of this strategy is to increase a nation's capital stock. This additive growth strategy essentially entails building more infrastructure; ― more roads, more dams, more bridges, more low-cost houses, more power stations, more waterways, more railway lines, more industrial parks, more office complexes, etc. ― in a bid to: 1) Create employment through large scale construction projects; 2) Stimulate aggregate demand through increased government spending; 3) Reduce the costs of doing business by eradicating infrastructural deficits and the bottlenecks they create, and; 4) Improve the populace's living standards by availing better amenities.

- Stage 4 - Innovation: This strategy entails purposely increasing the productivity of a nation's factor endowment (land and labor) and its capital stock. Otherwise put; it centers upon getting more outputs per unit of factor input. This growth strategy requires: 1) A critical mass of tertiary-educated people who are equipped with creative problem solving skills; 2) Public funding of basic research; 3) Strong inter-linkages between research institutions and industry; 4) A culture which is open to new ideas and creative exchange; 5) Strong institutions of intellectual property protection; 6) Incentives - an economic structure and tax code that allows innovators to earn outsize returns; 7) A culture with a positive attitude towards endeavor and failure; 8) An immigration policy that allows a country to absorb talented individuals from other parts of the world; etc. Clearly, this is the most obstreperous growth strategy; creating an assemblage of the precursors of innovation won't necessarily guarantee its occurrence.

Employing Stage 1-to-3 growth strategies is known, in economic parlance, as primitive resource accumulation. It is the growth strategy that the Soviet Union employed in its high growth phase in the 1960s, and; it is the strategy that China has employed from the late 1970s to date. Evidently, it is the most obvious, and least difficult growth path for African countries to follow.

In practice, there is no pure Stage 1, Stage 2, Stage 3 or Stage 4 African country. African countries tend to concurrently straddle across multiple stages. For instance, South Africa, the most advanced country on the African continent, is simultaneously a Stage 3 and Stage 4 country. Rwanda, is simultaneously a Stage 1, Stage 3 and Stage 4 country. While most other African countries are typically both Stage 1 and Stage 3 countries.

Owing to demographic forces, between 2015 and 2035 most African countries are set to become Stage 2 countries; i.e. countries that are supposed to grow via the rural-to-urban migration vector. This will occur atop:

- A thin industrial and service sector base in urban areas; i.e. a paucity of viable employment opportunities for rural-to-urban migrants;

- An urban infrastructural deficit and poor urban service delivery;

- A communal land tenure system, in rural areas, which encumbers consolidation of micro plots into more productive large-scale agricultural units.

As will be seen in subsequent sections of this blog post, this reality creates a myriad of internal security risks in African countries.

...The Water Scarcity Problem (Present to 2050; Probability = 70% to 100%)

"Humans have a natural loyalty to the things they were born into, the people and the places. Loyalty to a tribe, a city, or a nation is natural to people. In our time, national identity matters a great deal. Geopolitics teaches that the relationship between these nations is a vital dimension of human life, and that means that war is ubiquitous."

― George Friedman (The Next 100 Years)

Illustration 5 ― below ― depicts the per capita volume of Africa's internal renewable freshwater resources from 1967 to 2013:

|

| Illustration 5 (click on illustration to zoom in) Adapted From: World Bank, 2015E |

As Illustration 5 ― above ― shows, Africa's freshwater resources have been on a steady decline from 1967 to 2013.

A projection which assumes an African population growth rate of 2.31% per year and fixed total internal renewable freshwater resources (at 13,279,351,672,860.90 cubic meters) yields Illustration 6 ― below:

|

| Illustration 6 (click on illustration to zoom in) Adapted From: World Bank, 2015E [4] |

As Illustration 6 ― above ― shows, by 2050 Africa's collective internal renewable freshwater resources will stand at approximately 5,164.73 cubic meters per capita. This translates to roughly 3.17 times the US's consumption of water in 2011; a generous amount by all standards. However, as is the case with all averages, this popularized figure is misleading; it glosses over the reality. The visual aid in Illustration 7 ― below ― will be used to shed light on Africa's true water situation:

|

| Illustration 7 (click on illustration to zoom in) Adapted From: Google Earth Pro, 2015, and; UN Water, 2005 |

To expound on Illustration 7 ― above ―, the:

- Red Zone - North Africa and the Sahel Region: By 2050, the Sahara desert would have encroached 210 kilometers into the Sahel region (at an encroachment rate of 5 to 6 kilometers a year). Generally, the ecological degradation of the northern parts of the Sahel region will have an adverse impact on the food and water security of northern Senegal, southern Mauritania, central Mali, northern Burkina Faso, southern Algeria, Niger, central Chad, central and southern Sudan, and northern Eritrea. As it currently stands, the region's demand for water for irrigation matches the region's supply. Therefore, ceteris paribus, it is reasonable to assert that the water security of the region may be compromised by any attempt to expand the agricultural base in North Africa and the Sahel region.

- Green Zone - Horn of Africa: In low-to-middle income countries, like the ones in the Horn of Africa, 82% of the water is used for agricultural purposes. As it currently stands, this region's demand for water for irrigation also matches the region's supply. Therefore, as is the case for the Northern Africa, ceteris paribus, it is reasonable to assert that the water security of the region may be compromised by any attempt to expand its agricultural base.

- Yellow Zone - South Western Africa: South Western Africa has barely sufficient freshwater to fully satisfy irrigated crop demands. In fact, most of central and eastern South Africa, south eastern and north Eastern Zimbabwe, Swaziland, Lesotho and south western Mozambique has a low freshwater irrigation overdraft. Thus, it is reasonable to assert that the water security of the South Western Africa will be

compromised by any attempt to expand its agricultural base. Of all the vulnerable regions, South Western Africa has the most precarious water-security position. Clearly, this will make agriculture-led economic development difficult.

To sum up, the African regions or nations that have the highest water insecurity are: northern Senegal, southern Mauritania, central Mali, northern Burkina Faso, southern Algeria, Niger, central Chad, central and southern Sudan, northern Eritrea, Djibouti, Ethiopia, Somalia, central and eastern South Africa, south eastern and north eastern Zimbabwe, Swaziland, Lesotho and south western Mozambique.

To pinpoint the countries, from the given list, that have the highest vulnerability, it is necessary to assess their Vulnerability to Climate Change and their Change Readiness. This is done in Illustration 8 ― below:

|

| Illustration 8 (click on illustration to zoom in) Adapted From: ND, 2014 |

As Illustration 8 ― above ― shows, from the list of identified vulnerable countries, the countries that are most fragile include; Somalia [10], Eritrea, Zimbabwe, Sudan, Chad, Mauritania and Djibouti. Illustration 9 ― below ― shows the projections of the renewable internal freshwater resources of Somalia [10], Eritrea, Zimbabwe, Sudan, Chad, Mauritania and Djibouti between 2014 and 2050:

|

| Illustration 9 (click on illustration to zoom in) Adapted From: World Bank, 2015E, and Grid Arendal, 2001 [16] |

As Illustration 9 ― above ― shows:

- In 2022, Chad will become a water scarce country. This implies that a growing proportion of its budgetary expenditures will be devoted to importing food. Further, the country, if it is fiscally constrained and politically unstable in 2022, may need more donor support.

- Zimbabwe, Somalia, Eritrea and Djibouti and Sudan are already deep in the zone of water scarcity. For these countries, the situation is set to deteriorate progressively with the passage of time. Therefore, it is reasonable to assert that food imports will increasingly dominate their import ledgers. Evidently, this implies that these countries will increasingly become vulnerable to the gyrations of commodity markets. Thus, it is reasonable to expect social unrest in these countries whenever food prices spike sharply; the Malthusian dynamic. With the passage of time, the risk of unrest will increase sharply.

- Sudan is the most water insecure country in the group. Its current internal renewable freshwater resources stand at 80 cubic meters per capita, while South Sudan, its unstable breakaway republic has 2,270 cubic meters-worth of internal renewable freshwater resources per capita [12]. By 2050, Sudan's internal renewable freshwater resources will stand at 35.15 cubic meters per capita (i.e. slightly over Qatar's internal renewable freshwater resources in 2014). Before that point is reached, the government of Sudan will, if, in the unlikely scenario, the state-formation process in South Sudan yields a unitary state, seek a partnership with South Sudan for the joint development of South Sudan's water resources. However, in the most probable scenario, Sudan will seek to re-establish control of the water-rich regions of South Sudan including; the Upper Nile region, Al Wahdah, Warrap, Western Bahr el Ghazal, Northern Bahr el Ghazal, Western Equatoria, Al Buhayrat and Jonglei. This could be achieved by exploiting the ethnic fissures [20] in South Sudan, specifically by either: 1) Sponsoring sympathetic secessionist movement(s) in the named regions, and or; 2) Sponsoring both sides of any ethnic conflict that occurs in the named regions (this could be done until the regions degenerate and re-emerge as warlord-controlled fiefs that can be easily co-opted) [18]. Sudan's window of opportunity will present itself between 2016 and the early 2020s; i.e. when the rest of the world will be transfixed by the climaxing New Cold War ― simmering Russia-Nato tensions ― and China's economic sclerosis. Subsequent to this, tensions may rise between Sudan and its downstream White Nile neighbors; Ethiopia and Egypt. If Sudan fails to tap South Sudan's water resources before the end of the early 2020s, the country will, before the late 2020s, experience intense civil unrest that may lead up to a civil war. The unrest will start as either a small local water-related grievance, food riots or a Tahrir-Square-style uprising; which would rapidly escalate.

...The Ever-Present Pandemic Risk (Present to 2050; Probability 50% )

"If an intelligent extra-terrestrial was tasked with writing the encyclopaedia of life on this planet, twenty seven out of thirty of these volumes would be devoted to bacteria and viruses. With just a few of the volumes left for plants, fungi and animals, and, humans would just be a foot note... an interesting footnote... but a footnote nonetheless."

― Nathan Wolfe, Virologist

Most of the world's unknown viruses live in isolated pockets of the planet; i.e. in oceans and rain forests. Illustration 10 ― below ― shows the world's forest cover:

|

| Illustration 10 (click on illustration to zoom in) Adapted From: UNEP, 2005 |

As Illustration 10 ― above ― shows, most of Africa's unfragmented forest cover, i.e. the forest cover that has been least affected by human activities, can be found in the Democratic Republic of Congo, the Republic of Congo, Cameroon and Equatorial Guinea.

Otherwise expressed; the viruses that humans have had limited exposure to, may be found in the equatorial rain forests of the named countries. One can surmise that some of these viruses may, if they come into contact with human beings, be lethal. Hence, it is reasonable to argue that the deforestation of these areas could, at some point in in the future, unleash virulent viruses.

It would be difficult to forecast when such viruses will be encountered. However, what can be reasonably ascertained are the vectors that may land these viruses in major population centers.

For plausible scenarios on how these viruses may diffuse out into the world, see a blog post which I authored in 2013 which is titled From Nassim Taleb's Black Swans to Black Mambas: Scenarios on the Emergence and Development of Pandemics.

... The Technological Dystopian Scenario (Present to 2050; Probability = 80% to 100%)

"The moon is the first milestone on the road to the stars."

― Arthur C. Clarke

To restate the basis of Africa's relationship with the rest of the world:

Throughout the sweep of African history, the basis of the continent's relationship with the rest of the world has been commodities; gold, ivory, rubber, commoditized labor (slaves), wheat, base metals, energy commodities and other soft and hard commodities. This assertion simply implies that: 1) All relations, past and present, between Africans and external parties are buttressed by external parties' need for African commodities, and; 2) Commodity markets are the channel through which world events and trends are transmitted to Africa.

Therefore, to forecast the events that will unfold on the African Continent, one would need to identify phase transitions in commodity markets. One such trend is NewSpace Mining.

This trend can best be described as the extraction of mineral resources from extra-terrestrial domains. It has been made possible by admixtures of technological advancements in Aerospace, Automotive, ICT and Biotech industries.

For the sake of simplicity, the NewSpace Mining trend will be explained by narrating the endeavors of a company which is called Planetary Resources. My narrative will draw from a 2014 blog post which is titled ZimAsset: The Hidden Link between Asteroids, Platinum Group Metals and a NewSpace Company:

In November of 2010, Planetary Resources was established by Peter Diamandis (of the X-Prize fame), Erick Anderson and Chris Lewicki. The company envisages to extract mineral resources from extra-terrestrial bodies, particularly near-Earth asteroids.

Near-Earth asteroids are equidistant from Earth as the Moon. There are estimated to be more than 10,758 near-earth asteroids. Interestingly, a subset of these asteroids travels in similar orbits, around the sun, as Earth. It is these particular asteroids that Planetary Resources seeks to tap.

Naturally, this begs the following question: How much mineral wealth is in one asteroid? Generally:

- An asteroid contains Platinum Group Metals. These minerals can be found at concentrations that average 10,000 times the concentrations of the richest platinum mines on Earth. To put this into context;

- An asteroid with a volume of approximately 2,500 cubic meters would have approximately USD600 billion-worth of Platinum Group Metals (valued at current prices). This suggests that the average near-Earth asteroid has about USD240 million-worth of Platinum Group Metals per cubic meter.

- The Platinum Group Metals that are found on asteroids are twenty-five times the density of water.

- The non-Platinum-Group-Metal constituents of asteroids, i.e. the volatile materials on asteroids, are one of the most energy efficient materials known to mankind (when you break them down into hydrogen and oxygen). According to some estimates, asteroids may have up to USD50 million of rocket fuel per tonne.

Succinctly put; asteroids are replete with metals and energy materials. Evidently, Planetary Resources's endeavors are set to disrupt commodity markets inordinately. Indeed, this will have profound geopolitical implications that will be felt across the globe.

To estimate the approximate timing of the geopolitical implications of Planetary Resources's endeavors, it is necessary to have a cursory appreciation of the milestones the company has reached thus far, and, those it hopes to reach in the future. Illustration 11 ― below ― will be used to shed light on the chronological sequencing of the company's endeavors:

|

| Illustration 11 (click on illustration to zoom in) Adapted From: Anderson, 2014 |

On the 26th of July 2015, Planetary Resources successfully tested its asteroid prospecting equipment on orbit; it achieved its key milestone for 2015. In the 4th quarter of 2015, the company also received a legislative boost; President Obama signed the U.S. Commercial Space Launch Competitiveness Act (H.R. 2262) into law. The act recognizes U.S. citizens' right to own the asteroid resources they obtain. Thus, it is reasonable to assert that Planetary Resources is set to deliver its first mineral rights to a customer in 2017 (refer back to Illustration 11).

Hence between the mid-to-late 2020s, one can reasonably expect the impact of Planetary Resources's operations to be felt in global commodities markets. To answer the question of which African countries will be disrupted in the mid-to-late 2020s, Illustration 12 ― below ― will be used:

|

| Illustration 12 (click on illustration to zoom in) Adapted From: US Geological Survey, 2015 |

As Illustration 12 ― above ― shows, South Africa is the largest exporter of platinum in the world and Zimbabwe is the third largest exporter of platinum in the world. Hence, it is reasonable to assert that Zimbabwe and South Africa's platinum mining sub-sector will start to experience viability problems between the mid-to-late 2020s.

Naturally, this begs the question: 'To what extent will the platinum sector problems disrupt the mainstream economies of the named countries?' Illustration 13 ― below ― will be used to answer the question:

|

| Illustration 13 (click on illustration to zoom in) Adapted From: US Geological Survey, 2015, and; World Bank, 2015 |

As Illustration 13 ― above ― shows:

- Platinum exports accounted for 4% of Zimbabwe's GDP in 2014.

- Platinum exports accounted for 1.50% of South Africa's GDP in 2014.

Hence, it is reasonable to assert that both Zimbabwe and South Africa will, owing to falling platinum prices between the mid-to-late 2020s, endure economic recessions.

Of the two, Zimbabwe's recession will be the most acute. Thus, it is reasonable to argue that the pressures that the recession generates will shape the outcome of the country's 2028 elections. In South Africa, as has been observed in previous commodity market dislocations, the economic recession will fuel public unrest either in the form of pockets of strikes, ethnic violence or anti-immigrant pogroms.

Of the two, Zimbabwe's recession will be the most acute. Thus, it is reasonable to argue that the pressures that the recession generates will shape the outcome of the country's 2028 elections. In South Africa, as has been observed in previous commodity market dislocations, the economic recession will fuel public unrest either in the form of pockets of strikes, ethnic violence or anti-immigrant pogroms.

***

...The 1980s Redux: The Balance of Payments Blip (Late 2010s to early 2020s; Probability = 80% to 100%)

"A large increase in credit that isn’t matched by a similar rise in GDP or income is likely generating insufficient returns that one day will turn into losses"

― Charlene Chu

"As we have seen in recent crises, private risk taking and debt are socialized when a crisis occurs. So, even when public deficits and debt are low before a crisis, they can rise sharply after one erupts. Governments that looked fiscally sound suddenly appear insolvent."

― Nouriel Roubini

"The fact is there are few significant capital markets, their [frontier markets'] capacity to absorb inflows is limited, and they have a tendency to overheat when they try to absorb more than a modest amount of capital."

― Jim Rickards (The Death of Money)

By independence-era standards, the years from 1998 to 2010 were largely a period of incomparable joyous social development: they were a period of tranquility restored; of debt-burdens tamed; of dynamism unleashed, and; of economic vitality restored. It was once again ― as on the eve of independence ― morning; African countries felt young again and revived. Everything seemed to lay before them.

The main driver of this period of florescence was China's voracious appetite for commodities.

Between 2007 and 2015, some Sub-Saharan African countries took advantage of the era of record-low global interest rates ― which had been ushered-in by the monetary easing that ensued the global financial crisis ― by issuing Euro-bonds to fund various projects. Table 1 ― below ― lists some of the countries that recently took the great leap:

|

| Table 1 (click on table to zoom in) Adapted From: Bloomberg Data, 2015; CBonds Financial Information, 2015, and; World Bank Data, 2015 |

As Table 1 ― above ― shows, the top five issuers of Eurobonds, i.e. the countries that recently borrowed the highest proportions of their respective GDPs at the time of debt issuance, are:

- Gabon;

- Zambia;

- Ghana;

- Senegal, and;

- Rwanda.

In 2015, both Ghana and Zambia experienced fiscal strains owing to low gold prices and a weakening Chinese economy (low copper prices). Hence, it is reasonable to assert that this vulnerability predisposes them to deterioration of their respective balance of payments positions when US interest rates start to re-normalize; i.e. between 2016 to 2018.

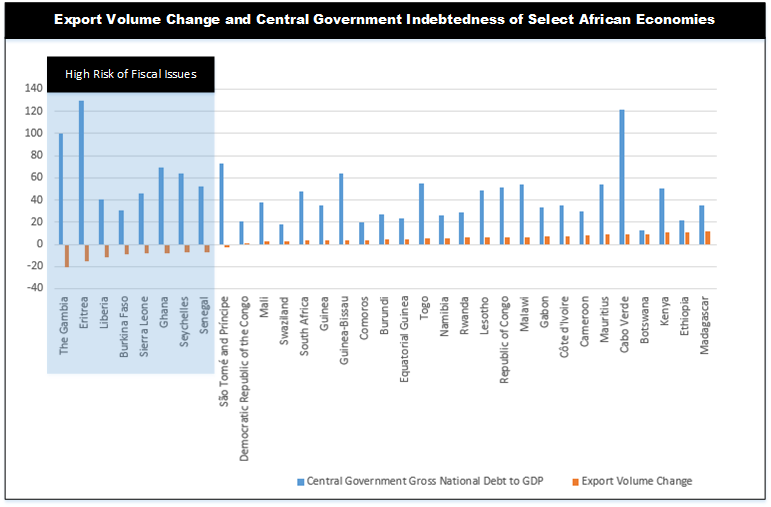

Illustration 14 ― below ― shows the central government indebtedness ratios and change of exports of select African countries in 2015:

|

| Illustration 14 (click on illustration to zoom in) Adapted From: IMF, 2015 |

In addition to their foreign currency and gold reserves, countries use proceeds from exports to settle their external liabilities. Thus, it is reasonable to assert the following: changes in export volumes reflect a country's ability to service its external debt; a positive change in exports reflects an increasing ability to service debt; while a negative change in exports reflects diminishing ability to service debt.

As Illustration 14 ― above ― demonstrates, like its fellow heavy-borrower Ghana, Senegal's exports fell in 2015. Hence, it is reasonable to assert that the country's ability to service its debt has diminished. Thus, it is reasonable to assert that the country is also highly vulnerable to being derailed by US interest rate hikes between 2016 and 2018.

To sum up, the countries that have the highest likelihood of developing fiscal issues between 2016 and 2018 are: Ghana, Zambia and Senegal.

To answer the question of which countries have the highest likelihood of developing fiscal issues in the post-2018 time-period, one has to examine each country's respective Current Account Balance and Government Budget Balance. To aid this endeavor, Illustration 15 — below — will be employed:

|

| Illustration 15 (click on illustration to zoom in) Adapted From: IMF, 2015, and; Trading Economics API Data, 2015 |

As Illustration 15 — above — shows the countries with twin deficits, i.e. high vulnerability to changes in the macro environment, are:

- Ghana

- Kenya

- Senegal

- Tanzania [21]

- Rwanda

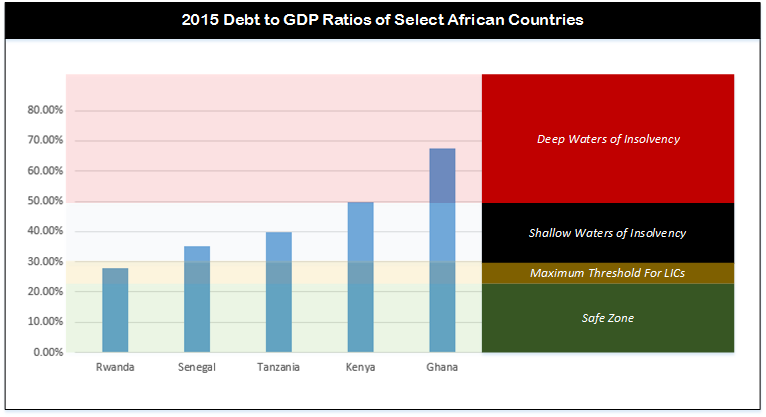

To pinpoint the countries with the highest vulnerability, i.e. the countries without enough legroom to refinance themselves out of problems, one would need to examine the Debt-to-GDP ratios of the above-named nations. Illustration 16 — below — will aid the endeavor:

|

| Illustration 16 (click on illustration to zoom in) Adapted From: Trading Economics API Data, 2015 |

As Illustration 16 — above — shows:

- Rwanda is the only country in the group with a Debt-To-GDP ratio that falls within the Club of Rome / IMF maximum Debt-To-GDP threshold for low-income countries. It has enough legroom to refinance itself out of problems.

- Although the problems are not yet visible, Senegal, Tanzania and Kenya are already in the shallow waters of the zone of insolvency; their solvency situation will deteriorate rapidly between 2018 and 2020 — when China's non-performing loan cycle reaches a crescendo.

- Ghana is already in the trouble zone. If the Asian Currency crisis is used as a template, it is reasonable to assert that Ghana's foreign currency reserves will continue to be depleted until interest rates are raised to the up to the point that induces inward capital flows. No one knows the interest rate that will do this. However, what is certain, is: between 2016 and 2018, when global interest rates start to normalize, Ghana will experience renewed pressures; inward capital flows that, ceteris paribus, would have been induced by previous Ghanaian rate hikes will ebb as they chase the increasing yield in more stable investment destinations. Hence, Ghana will be forced to endure another cycle of sharp successive rate increases between 2016 and 2018. Further, increases in global interest rates will raise Ghana's debt service costs; which would, in turn, further-deplete the nation's reserves. This would create more downward pressure on the Cedi. Furthermore, gold accounts for close to 44% of Ghana's exports; it is Ghana's major foreign currency earner. Thus, it is reasonable to assert that Ghana would face added pressure as the price of gold weakens — owing to a stabilizing global economic outlook — between 2016 and 2018. This vulnerability will spill into the 2020s; it can only be meaningfully eradicated by a protracted period of high gold and oil prices and or partial debt forgiveness.

***

To close off, at the most fundamental level, interest rates are a function of; the prevalent stage of the business cycle, the demand for money and the supply of investible assets in an economy.

The demographic structure of a society is a key determinant of its supply investible assets; particularly, the proportion of the populace in the Saver Generation (50 to 64 years of age). Typically, the 50-to-64 age bracket is the source of 70% of investible assets and taxes in developed economies.

Globally, the current Saver Generation are post-WWII Baby Boomers. As a generation, they account for between 20% and 35% of the population of G8 nations; i.e. a significant share of the populace of developed nations.

Illustration 17 — below — shows the trajectory of US Total Defined Contribution Assets as the Baby Boomer generation has aged [28]:

|

| Illustration 17 (click on illustration to zoom in) Adapted From: Investment Company Institute, 2015 |

As Illustration 17 — above — shows, the total of US Defined Contribution Assets has grown as the Baby Boomers have aged. Unfortunately, this trend will not persist ad infinitum; when the Baby Boomers enter into retirement — between 2020 and 2022 — total US Defined Contribution Assets will fall. [27]

Otherwise expressed; the supply of investible assets will dwindle between 2020 and 2022 in the US (and other G8 economies). Consequently, there will be a sharp uptick of global interest rates in the post-2022 time period; i.e. when the Eurobonds of African issuers start to mature (refer back to Table 1).

Hence, it is reasonable to expect some of the issuers of Eurobonds to be crushed by the growing debt service burden. As Illustration 15 showed, the countries that are most vulnerable to macro changes, like a sharp increase in interest rates, include:

- Ghana

- Kenya

- Senegal

- Tanzania [21]

- Rwanda

...The Demographic Conflagration (2021 to 2035; Probability = 50% to 80%)

"The perversity of the universe tends towards a maximum. / Anything that can go wrong, will — at the worst possible moment."

— Murphy's Law or Finagle's Law

Proponents of the Africa Rising narrative tout Africa's youthful population as an advantage; a factor endowment to behold; a source of future economic vitality; a potential demographic dividend. This is true, but it is not the complete story.

The metaphor of the coin in Illustration 18 ― below ― will be used to elucidate all aspects of the African demography story:

|

| Illustration 18 (click on illustration to zoom in) |

The coin in Illustration 18 ― above ― represents Africa's demographic structure. It is common knowledge that the continent's demographic structure is youth-heavy; it had an average age of 18 years in 2012. This youthful population could be a growth-enhancing opportunity; represented by the dollar sign on the "heads-side" of the coin in Illustration 18; it could earn Africa a demographic dividend. Or, it can be a curse; represented by the obscured "tails-side" of the coin in Illustration 18; it could represent demographic structural risk. To establish if Africa, as a continent, is utilizing its youthful labor endowment well, Illustration 19 ― below ― will be used:

|

| Illustration 19 (click on illustration to zoom in) Adapted From: World Bank, 2015 |

As Illustration 19 ― above ― shows, during the last 23 years, the labor force participation rate of African young males (aged 15 to 24 years old) was on a steady downtrend. Otherwise put; an increasing proportion of African young males is not entering the workforce; they are idle. An increasing unemployment rate or a reducing labor force participation rate for young males indicates rising risk of societal instability. Succinctly: the demographic coin in Illustration 18 ― above ― is biased to land on the "heads-side"; with the "tails-side" facing-up.

To assess the countries that have a high risk of demographically-induced instability, Table 2 ― below ― will be used:

|

| Table 2 (click on table to zoom in) Adapted From: Korotayev et al., 2011 [15] |

Table 2 ― above ― shows the urban youth population growth rate in different African countries. When Korotayev et al. (2011) teased data from around the world, they found that:

"The probability of major internal violent conflicts in countries with very low young urban population growth rates (less than 15 percent increase per 5 years) was very low. For countries with intermediate values of these rates (20–30 percent increase per 5 years) the probability of such conflicts was close to 50 percent. However, even for this group of countries there was not a single occurrence of a particularly violent internal political upheaval in the given period. In countries with high young urban population growth rates (30–45 percent increase per 5 years) the probability of avoiding major political upheavals falls down to a very low level (about one chance out of four). Additionally, the probability of a particularly violent civil war becomes very high in these countries (also about one chance out of four). In countries in which the young urban population growth rates were very high (45 percent increase in 5 years) not a single one managed to avoid major political shocks. The risk of a particularly violent civil war was very high for these countries (about one chance out of two)."

Throughout the world, it is widely accepted that societies that are not based on consent and equality lack durability. Inequality, when it exceeds a GINI Index of 0.4 tends to correlate with a high risk of instability. Further, when:

- A nation's Actual GINI Index approaches the nation's Maximum Feasible GINI Index (G*), a nation's risk of instability becomes elevated.

- A low income nation's Inequality Extraction Ratio approaches 1, the nation's risk of instability becomes elevated.

Therefore, to pinpoint the constituents of Table 2 ― above ― that are predisposed to various forms of Instability, Illustration 20 ― below ― will be used:

|

| Illustration 20 (click on illustration to zoom in) Adapted From: Milanovic, 2012; World Bank, 2015C, and; World Bank 2015D |

As Illustration 20 ― above ― shows, the countries from Table 2 that have: 1) a GINI Index greater than 0.4; 2) an Actual GINI Index which is close to the Maximum Feasible GINI Index (G*), and; 3) an Inequality Extraction Ratio which is closest to 1, are:

- Rwanda

- Kenya

- The Gambia

- Malawi

- Mozambique

- Chad

- Uganda

- The Democratic Republic of the Congo

In these countries, politically weak locals and foreigners may face the risk of asset expropriation. In the case of politically weak locals, they may decide, during each country's respective period of maximum structural demographic risk, to seek remedy through violence.

To establish the countries that are most predisposed to this form of unrest, Illustration 20 ― below ― will be used:

|

| Illustration 21 (click on illustration to zoom in) Adapted From: Heritage Foundation, 2015 |

As Illustration 21 ― above ― shows, the countries with the highest risk of unrest which is fueled by an incident of expropriation, include:

- The Democratic Republic of the Congo.

- Chad.

- Uganda.

- The Gambia.

The probability of these forms of unrest eventuating ranges between 50% and 80%; the time to expect these forms of unrest ranges between 2016 to 2030.

***

To close off, while democracy does not directly bolster economic growth, it does have one pivotal advantage: It mitigates the risks of violent transitions of power.

In Illustration 22 ― below ― Freedom House's Democracy Ratings and the metrics in Illustration 20 ― above ― are blended in a proprietary index to establish each country's risk of violent power transitions:

|

| Illustration 22 (click on illustration to zoom in) Adapted From: Milanovic, 2012; Freedom House, 2015, and; Korotayev et al., 2011 |

As Illustration 22 shows, the countries with the highest probability of experiencing violent transitions of power include:

- Niger (between 2021 and 2030).

- Uganda (between 2021 and 2030).

- Malawi (between 2011 and 2020).

- Kenya (between 2021 and 2030).

- Burkina Faso (between 2021 and 2030).

...The Great Transition of China and its Shockwaves (Late 2010s to Early 2020s; Probability = 70% +) [24]

"China is inherently unstable. Whenever it opens its borders to the outside world, the coastal region becomes prosperous, but the vast majority of Chinese in the interior remain impoverished. This leads to tension, conflict, and instability. It also leads to economic decisions made for political reasons, resulting in inefficiency and corruption."

― George Friedman (The Next 100 Years)

According to George Friedman, China is on track to experience an economic slowdown between the late 2010s and the early 2020s. He identifies the key vulnerabilities of China as follows:

"China appears to be a capitalist country with private property, banks, and all the other accoutrements of capitalism. But it is not truly capitalist in the sense that the markets do not determine capital allocation. Who you know counts for much more than whether you have a good business plan. Between Asian systems of family and social ties and the communist systems of political relationships, loans have been given out for a host of reasons, none of them having much to do with the merits of the business. As a result, not surprisingly, a remarkably large number of these loans have gone bad — “nonperforming,” in the jargon of banking. The amount is estimated at somewhere between $600 billion and $900 billion, or between a quarter and a third of China’s GDP, a staggering amount [2008 to 2009 numbers]. These bad debts are being managed through very high growth rates driven by low-cost exports. The world has a huge appetite for cheap exports, and the cash coming in from them keeps businesses with huge debts afloat.

But the lower China sets its prices, the less profit there is in them. Profitless exports drive a giant churning of the economic engine without actually getting it anywhere. Think of it as a business that makes money by selling products at or below cost. A huge amount of cash flows into the business, but it flows out just as fast."

To help place into context the potential implications of China's non-performing loan problem, Table 3 ― below ― will be used:

|

| Table 3 (click on table to zoom in) Adapted From: Bass, 2015 |

In 2015, China's banking system had assets of approximately USD 31,000,000,000,000.00. Hence, as Table 3 ― above ― shows, if [14]:

- China's non-performing loans stand at their general all-time historical average, 19%, the nation's USD 3.2 to 3.5 trillion (forex) reserve arsenal would be insufficient to bail out its banks.

- China's non-performing loans stand at their 1997-Asian Financial Crisis level, 25%, China's non-performing loans are 2.15 times its reserves.

- China's non-performing loans stand at their general banking crisis average, 35%, China's non-performing loans are 3.01 times its reserves.

The exercise that was conducted above simply serves to highlight the magnitude of China's non-performing loan problem; it is of colossal proportions.

As was stated in the section which is titled Basic Element 1: How The World (and Africa) Really Works:

"Throughout the sweep of African history, the basis of the continent's relationship with the rest of the world has been commodities; gold, ivory, rubber, commoditized labor (slaves), wheat, base metals, energy commodities and other soft and hard commodities. This assertion simply implies that: 1) All relations, past and present, between Africans and external parties are buttressed by external parties' need for African commodities, and; 2) Commodity markets are the channel through which world events and trends are transmitted to Africa."

When the Chinese economy tailspins, its demand for commodities will dwindle. Hence, it is reasonable to assert that the dislocation of the Chinese economy will be felt in the commodities export ledgers of African countries. Illustration 23 ― below ― shows the African countries that will feel the impact of China's crisis most:

|

| Illustration 23 (click on illustration to zoom in) Adapted From: Bloomberg, 2015, and; IMF, 2015 |

In Illustration 23, a nation's exposure to China is calibrated using the Exports-to-China as a Percentage of Total Exports ratio. As Illustration 23 ― above ― shows, the African countries that have the highest exposure to China are:

- The Republic of Congo.

- Angola.

- Mauritania.

- Zambia.

- South Africa.

Therefore, between the late 2010s and early 2020s one can reasonably expect these countries to endure economic recessions that stem from a Chinese economic crisis. In some of these countries, political upheavals will arise. Regrettably, the prosaic methods for stamping out the-said unrest will entail violations of human rights and civil liberties.

...The Aftermath of the Second Cold War: The Great Geopolitical Realignment (2050; Probability = 100%)

"The question that will come to the fore in 2040 will be this: What will be the relationship between the United States and the rest of the world? On one level, the United States will be so powerful that virtually any action it takes will affect someone in the world. On the other hand, the United States will have such power, particularly after the Russian retreat and Chinese instability, that it can afford to be careless. The United States is dangerous in its most benign state, but when it focuses down on a problem it can be devastatingly relentless."

― George Friedman (The Next 100 Years)

By the mid-2030s, the horrors that will befall the African continent in the 2020s would have partially fulfilled themselves. African countries will emerge from the decade leading-up to 2030 as Stage 1-Stage 2-Stage 3 economies ― refer back to Illustration 4.

In the 2030s, Africa will be bruised by a myriad of social, economic and political maladies. Throughout the continent, the confidence of nations will evaporate; the problems will just be too numerous and too intractable for African supranational organizations alone to tame. Hence, the death of the "African solutions to African problems" mantra of the 2010s. In the 2030s, it will be a bygone relic of a failed age of pan-Africanism.

In the mid-2020s to early 2030s, African countries will, as individuals, reach out to the world for help. But who will be there to help them? The retreat of Russia [1] and the economic sclerosis of China [2] in the 2020s rule both titans out.

Owing to historical ties that date back to the age of the Ottoman Empire and religious bonds, North African countries will tend to naturally gravitate towards an ascendant Turkey; the natural leader of the Sunni Muslim world.

Sub-Saharan Africa will naturally gravitate towards the United States, which will emerge from the 2020s bolder than ever.

This implies two things:

- Washington Consensus: The Washington Consensus will have primacy in the organization of the affairs of Sub Saharan African countries.

- Renewed Ethnic Tensions: The 2030s will be an era of liberalization in Sub-Saharan Africa. In some countries with a deep history of ethnic divisions, freedom of speech would be tantamount to lighting up a powder keg. It will create new dangerous realities; a dynamism that could lead to disaster [17]:

Illustration 24 ― below ― will be used to expound on Renewed Ethnic Tensions:

|

| Illustration 24 (click on illustration to zoom in) Adapted From: Sundberg, Ralph, Kristine Eck and Joakim Kreutz, 2012 |

In Africa, a good guide for where informally organized ethnic violence may occur in the future is where it has occurred in the past. Illustration 24 ― above ― shows the frequency of informally organized ethnic violence in different African countries.

According to Illustration 24 ― above ―, the countries with the highest incidents of informally organized ethnic violence include; Nigeria, Sudan, Ethiopia, Kenya, Somalia, The DRC and South Sudan. Net the countries that will be in the Turkish orbit (i.e. Sudan), the countries that may be destabilized by increasing liberalization in the 2030s are:

- Nigeria.

- Ethiopia.

- Kenya.

- Somalia.

- The DRC.

- South Sudan.

Between the 2030s and 2050s, four African nations will start to emerge as economic titans owing to strong demographic tailwinds [23]. Illustration 25 ― below ― reveals these countries:

|

| Illustration 25 (click on illustration to zoom in) Adapted From: The Economist, 2015 |

As Illustration 25 shows, the African countries that will have large populations in 2050 include:

- Nigeria (already the largest economy on the African continent).

- The Democratic Republic of the Congo [22].

- Ethiopia.

- Egypt.

Owing to increased aggregate domestic consumption, in nominal terms, these countries will have some of the largest economies on the African continent. However, on a per capita basis they will remain low-to-middle income Stage 2 to 3 countries.

[2] For more details see Chapter 5 of the-said text which is titled China 2020: Paper Tiger.

[3] The confrontation was recently sparked, on the 24th of November 2015, by the downing of a Russian fighter jet near the Turkey-Syria boarder. For more details see Chapter 8 of the-said text which is titled A New World Emerges.

[4] These projections exclude the 0.66 million km3 (0.36–1.75 million km3), groundwater reserve ― 100 times Africa's renewable surface freshwater resources ― that was discovered by the British Geological Survey because most of its water resources are largely difficult to extract.

[5] The history is presented in a tome which is entitled The Fortunes of Africa: A 5000-Year History of Wealth, Greed, and Endeavor

[6] This is particularly true in conditions of hardship.

[7] An illuminating excerpt from the The Revenge of Geography: What the Map Tells Us About Coming Conflicts and the Battle Against Fate by Robert D. Kaplan: "Mountains are a conservative force, often protecting within their defiles indigenous cultures against the fierce modernizing ideologies that have too often plagued the flatlands, even as they have provided refuge for Marxist guerrillas and drug cartels in our own era.1 The Yale anthropologist James C. Scott writes that “hill peoples are best understood as runaway, fugitive, maroon communities who have, over the course of two millennia, been fleeing the oppressions of state-making projects in the valleys.”2

[8] This relationship was popularized by, and termed "creditism", in Richard Duncan's book which is titled The New Depression: The Breakdown of the Paper Money Economy.

[9] China has a mercantile foreign policy: it will work with any government regardless of the government's democratic credentials.

[10] Somalia was not shown in illustration 8 because it had a scale-tipping reading.

[11] This doesn't rule out mutations of known viruses being discovered.

[12] Note: this estimate does not factor in the effect of desertification.

[13] Most of the internal renewable freshwater resources are groundwater and seasonal rivers.

[14] Historical non-performing loan averages were extracted from Red Capitalism: The Fragile Financial Foundation of China's Extraordinary Rise by Carl Walter and Fraser Howie.

[15] The asterisk simply shows that a nation is in East or Central Africa; the most conflict-prone region of Africa.

[16] Reliable estimates for Mauritania could not be found at the time of publishing this blog post.

[17] In an environment with deep ethnic hostilities, freedom of speech will increase the probability of people saying things that people from other ethnicities may find offensive. And, this could trigger waves of unrest.

[18] This may be the main driver of the current bout of ethnic unrest in South Sudan.

[19] Robert D. Kaplan's definition of a culture: "A culture is the shared experience of a very large group of people, in a particular territorial setting over hundreds and thousands of years, that leads to commonalities (of music, art, points of view, fears, biases, etc.)"

[20] My opinion: South Sudan has 60 different ethnic groups that speak close to 80 different languages. Prior to seccessation from Sudan, the only thing that gave these disparate peoples a sense of a shared fate was institutionalized discrimination and persecution; to the Northerners they were all abd (slaves) who had a subordinate status. Subsequent to the formation of South Sudan, the sense of a shared destiny appears to have vanished; there is the sense, among some sections of South Sudan's smaller ethnic groups, that they are being subordinated by larger ethnic groups (i.e. by the Dinka, Nuer and Shilluk). Otherwise put, ethnic fissures are already beginning to assert themselves. Abba Eban once said that "a nation's security is not only or primarily a function of its territorial size, it is a function of its inner cohesion, of the harmony that makes people want to live together under the same flag and to revere the same anthem, and to nourish the same memories, and to express the same hopes. And in the absence of that unifying voluntary energy, no national society can be assured of any degree of stability". It can be argued that South Sudan currently lacks inner cohesion; it is not a state. Further, a look at the map of South Sudan reveals that the density of major freeways is highest in the South West, i.e. near Juba. This may suggest that the administrative reach of the South Sudanese authorities ends where the major road network ends, and; that the fate of the regions outside this network of roads is open to 'negotiation'.

[21] Postscript 5/12/2015: According to Reuters, On the 4th of December 2015, the Tanzanian president, John Magufuli gave tax-evaders one week to pay-up what they owe or face prosecution. Generally, countries do not take such measures unless they are experiencing severe fiscal issues that need to be addressed urgently.

[22] Postscript 6/12/2015: The biggest surprise on the list is the DRC. It needs some justification. The DRC is a large, centrally-placed natural resource-rich country [with newly discovered oil reserves and a host of other minerals]. Further, it is situated on the Atlantic coast of Africa (i.e. the US's neighborhood). Therefore, it is reasonable to argue that the US has vital interests in the DRC, they can be abbreviated as follows: 1) A relationship with the DRC will allow the US to access minerals that drive the modern economy (coltan) and oil from a more proximate location, and; 2) A relationship with the DRC will allow the US ― a maritime superpower ― to access the DRC's maritime installations (ports) - a proactive security measure that will prevent rival ascendant powers ― Turkey, Japan and Poland ― from projecting their influence into the South Atlantic region. These vital interests will compel the US to establish a relationship, in the 2020s, with the next government of the DRC. If the US doesn't do this, either Turkey, Japan or Poland will. A relationship with the US or any emerging power will, for the DRC, open up new markets, facilitate technology transfers and avail access to capital and expertise. This is analogous to the impact that a relationship with the US had on South Korea during the latter half of the 20th century. Simply put; a relationship with the US will unleash a tidal wave of growth in the DRC. Further, a host of sub-Saharan African countries are set to benefit, through electricity, from the Grand Inga dam project. Otherwise put, they now have vital interests in the DRC and they will, as they (South Africa and Tanzania) are currently doing, secure the volatile Kivu region, until the DRC is in a position to establish a formal allegiance with the US. Furthermore, international opinion makers, media and aid organizations are now intensely focused on highlighting the true drivers of the violence in the DRC. Otherwise put, there now is a convergence of interests that will stabilize the DRC. In 2050, the DRC is projected to have a population of 194 million people. If one postulates that all of these people will be at the world poverty datum line with a consumption of rate of $1.25 per person per day; the DRC's household consumption component of GDP will stand, in current dollar terms, at USD 88.5 billion; i.e. just over Oman's GDP in 2014 or roughly over Sudan's ― the 7th largest economy in Africa ― GDP in 2014.

[23] Strong Demographic Tailwinds and how they elevate the risk of collapse: According to Peter Turchin, "Stability and internal peace bring prosperity, and prosperity causes population increase. Demographic growth leads to overpopulation, overpopulation causes lower wages, higher land rents, and falling per capita incomes for the commoners. At first, low wages and high rents bring unparalleled wealth to the upper classes, but as their numbers and appetites grow, they also begin to suffer from falling incomes. Declining standards of life breed discontent and strife. The elites turn to the state for employment and additional income, and drive up its expenditures at the same time that the tax revenues decline because of the growing misery of the population. When the state’s finances collapse, it loses the control of the army and police. Freed from all restraints, strife among the elites escalates into civil war, while the discontent among the poor explodes into popular rebellions."

[24] Postscript 10/12/2015: If the sclerosis of China seems implausible, consider this latest prediction from George Friedman's latest forecast: "In Asia, as the decline of China’s competitiveness in the export market continues, high unemployment will become a significant challenge to the Chinese president. The regime will attempt to survive the economy’s downward spiral by tightening its grip on power and sliding back into dictatorship. However, the regional divergences in China are too widespread and not easily suppressed by dictatorship. Therefore, by 2040, China will see a return to regionalism, accompanied by turmoil. As China weakens, a power vacuum will emerge in East Asia, which will be filled by Japan. By 2040, Japan, with its enormous economy and substantial military capabilities, will become the leading East Asian power."

[25] Postscript 12/12/2015: This growth strategy requires funding from taxes and or deep and liquid local capital markets, or, finances from international fixed income markets. Most African countries have narrow tax bases; thus, this implies that tax revenues cannot be used to fund Africa's USD 100 billion+ annual infrastructure investment requirement. As far as local capital markets are concerned, most African countries also have low savings rates. Thus, their respective local capital markets tend to be too small to finance their infrastructural needs. Hence, they are left with one viable alternative: international debt markets.

[26] Postscript 13/12/2015: This state of affairs has existed since 1945, i.e. when the Bretton Woods agreement was signed. The agreement effectively opened-up the U.S. markets to exports from all parts of the globe.

[27] The replacement generation of the Baby Boomers, Generation X, is not large enough to provide a comparable volume of investible assets.

[28] The US has the largest, most liquid and most sophisticated capital markets in the world.